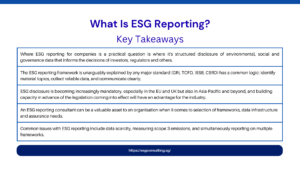

What Is ESG Reporting?

A practical guide for junior to mid-level finance and sustainability professionals

Understanding What Is ESG Reporting?

ESG reporting is the collection, disclosure and communication of the efforts of organisations in three non-financial areas – Environmental, Social and Governance. The first thing to know about what ESG reporting for companies entails is to realise that it is not just a box-ticking exercise but a way for companies to show that they are being held accountable by investors, regulators, employees and the general public. The necessity to produce credible, structured ESG disclosures has shifted from a “nice to have” to a “must,” and as disclosure mandates become more widespread and investor interest in sustainability practices grows, it is more important than ever.

What Is ESG Reporting for Companies — and Why Has It Become Non-Negotiable?

In the early days of corporate reporting, the annual report was essentially a financial document, detailing the revenue, costs, profits, and balance sheet position of the company. ESG reporting is a cornerstone expansion of that responsibility. An honest answer to the question “what is ESG reporting for companies in full?” is that ESG reporting is about recognising that companies impact and are impacted by much more than just the financial factors as traditionally reported in statements. Climate risk, labour practices, supply chain integrity, board composition, data privacy and community impact, etc., are all factors that need to be recognised.

Voluntary to mandatory disclosure has been the most prominent development in regulations over the last five years. The new Corporate Sustainability Reporting Directive (CSRD) of the European Union (EU) was adopted in 2024 and will impact thousands of companies, even those not based in the EU but that have operations in Europe. The European Union (EU) Corporate Sustainability Reporting Directive (CSRD) became effective in 2024 and will affect thousands of companies, including non-EU companies that have extensive operations in the EU. The International Sustainability Standards Board (ISSB) has also released IFRS S1 and S2, which are being adopted or adapted by various regulators in the UK, Australia, Canada and several Asian markets. In the business world, strategy, finance, or corporate affairs, knowing this is no longer an option.

ESG reporting is not just about compliance; it’s a way for investors to evaluate the long-term quality of a business. A growing majority of major asset managers today routinely incorporate ESG data into investment analysis procedures, and credit rating agencies have begun to begin incorporating ESG into their corporate creditworthiness assessments. Without coherent ESG disclosures, a company is at risk of losing access to some investment mandates, increased cost of capital, and talent as well – because tomorrow’s worker is more likely to turn down a job just as much as an investment.

How Is the ESG Reporting Framework Explained Across Different Standards?

Given that there are a number of different standards for ESG reporting, and each has a different approach, audience, and disclosure needs, the ESG reporting framework explained through any one of these standards can be intimidating and confusing for those new to the field. More practically, most professionals will find that there are a few dominant standards that they will need to come to understand, and it will be more helpful to understand how these standards interrelate than to master each one individually.

The Global Reporting Initiative (GRI) Standards are the most widely adopted reporting framework in the world, and have a stakeholder-centred approach, with a focus on the effects that the company has on society and the environment, rather than what is financially material to investors. The Task Force on Climate-related Financial Disclosures (TCFD) is a narrow but highly deep focus on climate risk, asking companies to report on governance, strategy, risk management, and metrics on four pillars structured around the problem. The IFRS Foundation also incorporates SASB (Sustainability Accounting Standards Board), which offers guidance on which of the ESG metrics are most likely to be financially material for companies in a specific industry, especially on investor-facing disclosures.

The IFRS S1 and S2 (published in 2023) are the largest recent developments in the ESG reporting framework and explainable landscape. They are intended to provide a set of global disclosures for investors, two of which were developed (S1 and S2) – the latter covering climate-related disclosures. The EU’s ESRS, which form the basis of the CSRD, are more extensive and detailed, and call for the disclosure of a wider set of topics, such as Biodiversity, Human Resources, Business Conduct, and require a principle of ‘double materiality’ — companies must identify the financial impact of ESG factors on their businesses, and the impact of their businesses on society and the environment. This is where an ESG reporting consultant can be of great help in negotiating these frameworks at the same time.

Major ESG Frameworks at a Glance

| Framework | Primary Focus | Who Uses It | Mandatory? |

|---|---|---|---|

| GRI Standards | The project highlights the importance of engaging stakeholders broadly in ESG | Global; all sectors | Voluntary (some jurisdictions) |

| TCFD | Risk & Opportunity: Climate Change-related Financial Risk & Opportunity | Listed companies, financials | In some markets, it is obligatory to have it. |

| SASB Standards | Comprehensive ESG data for the industry. | US-focused; investor audience | Voluntary |

| ISSB (IFRS S1/S2) | Investor-grade sustainability disclosure | Listed companies globally | Rapidly becoming mandatory |

| EU CSRD / ESRS | Comprehensive EU sustainability reporting | Large EU entities & others | These are required for in-scope companies. |

What Are the Five Core Components That Every ESG Report Must Address?

However it reports, a good ESG report will cover the five key elements. These collectively make up the structure of credible disclosure.

- Governance Structure: Each ESG report starts with governance – the way the board and management manage sustainability risks and opportunities. This covers board-level responsibility and integration for ESG topics, as well as executive bonus plans aligned to ESG performance and strategy, and risk management processes. Robust governance disclosures indicate that ESG is not only not contained in a corporate affairs team, but is also part of the way a company runs.

- Materiality Assessment: Materiality is a process of identifying those ESG topics that are material and for which disclosure should be made. There are multiple, different definitions of materiality, including financial materiality (which relates to impact on business value) and impact materiality (which relates to impact on people and planet), and all involve judgment and stakeholder engagement on the part of companies. A thorough materiality analysis provides the basis for a focused and credible report.

- Beyond Energy : Water, and waste, the key focus of most environmental disclosures is environmental data and targets: Greenhouse gas emissions Scope 1 (direct), Scope 2 (purchased energy), and Scope 3 (value chain). Science-based targets, accompanied by companies, are becoming more and more the norm, establishing a realistic decarbonisation path based on the scientific targets.

- Social and Workforce Disclosures: This includes a broad spectrum of disclosures including employee health and safety, diversity and inclusion disclosures, pay equity, supply chain labour standards and community engagement. Social data has historically not been as good as environmental data, in part due to its lack of standardisation and quantitative data. Investors and regulators are increasingly demanding that companies improve in this regard.

- Expectation for Third-party Assurance: Rapidly growing, as ESG reporting matures, calls for assurance and Data Integrity. Assurance – either limited or reasonable – is provided by an independent auditor, supporting confidence in the information presented and the method by which that information was created. A move towards assurance of ESG disclosures is underway in various regulatory frameworks, such as CSRD.

What Do Real Cases Reveal About the Challenges and Lessons of ESG Reporting?

Fewer companies have experienced several rounds of ESG reporting and, as such, the experience of those companies provides much more nuance and insight into the process than any document of the framework. The lessons are helpful for those who are developing this capability for the first time.

Elpida is widely recognized as one of the world’s leading corporate ESG reporters, cited as such by Unilever. The company initiated an integrated sustainability report in 2010 and published the Sustainable Living Plan, introducing sustainability outcomes and connecting business targets and sustainability outcomes. What set Unilever apart was the DNA test of sustainability data with the same rigour as financial data, an investment which demanded a significant investment in data systems and internal audit resources. The value was that it was credible: when they promised to measure the carbon footprint of its production, its supply chain, etc., they could do so without having to rely on data that was not fully guaranteed, which would be easier for investors and NGOs to dispute. For organisations just starting their reporting journey, the lesson is the infrastructure must be established before the disclosure can be effective – it is only as high quality as the underlying data.

A prime example of a warning message is the wave of greenwashing cases which regulators and investors have been going after over the last few years. A number of large financial institutions have been targeted for their public statements about ESG credentials of their investment products that were inconsistent with the underlying portfolio holdings, and/or the investment processes. In one high-profile example, a global asset manager was slapped with a hefty regulatory penalty for over-claiming the degree of integration of its ESG approach for several funds. The case reaffirmed the legal accountability on ESG reporting, similar to that of any other corporate reporting; misstatements of fact or even aspersions of fact have real consequences. The rules governing the substance of an ESG claim and its support with evidence are good practice and, indeed, a legal obligation for anyone making an ESG disclosure.

The third learning outcome is that of companies dealing with Scope 3 emissions, or the indirect emissions generated throughout a company’s value chain, such as from its suppliers and customers. While Scope 3 is the most complex and difficult to quantify, measure, and impact, it is often the biggest component of a business’ carbon footprint. A few big consumer goods and retail firms have admitted publicly that their Scope 1 and 2 efforts (those where they have achieved significant cuts) lag far behind their Scope 3 journey (where progress has been much slower). An open admission of that divide – and the clear and viable steps to close the divide – is a sign of reporting maturity. Businesses with only half the data are the ones that are coming under the spotlight from investors and analysts because they don’t cover data that they can’t yet measure.

What Does the ESG Reporting Process Look Like From Start to Finish?

It is key to understand the end-to-end workflow for organisations that are just beginning ESG reporting (or want to boost the rigor of a process they are implementing). It is most beneficial for an ESG reporting consultant to be involved at the scoping and materiality stages where important decisions are made on selection of the ESG framework and prioritisation of topics that have the biggest downstream impact.

The Six-Phase ESG Reporting Workflow

| Phase | Key Activities | Output |

|---|---|---|

| 1. Define Scope & Purpose | Identify reporting standard, audience, and materiality boundary | Document describing the reporting requirements and scope. |

| 2. Materiality Assessment | Involve stakeholders and uncover ESG topics relevant to business and society; | Materiality matrix |

| 3. Data Collection | Collect quantitative data (emissions, energy, workforce) and qualitative data disclosure | Raw data inventory |

| 4. Gap Analysis | Compare and contrast collected data with framework requirements; identify gaps | Gap report and prioritise actions |

| 5. Draft & Review | Create narrative, disclosures and data tables; internal review and sign-off | Draft ESG report |

| 6. Assurance & Publication | Split the work of publishing and distributing into third-party assurance (limited or reasonable). | Assured, final ESG report |

One aspect of phase two – the materiality assessment – requires careful attention as it is the aspect where many organisations underinvest. A superficial materiality process, which is done internally without true participation of stakeholders, is likely to create a list of topics that are already being addressed by the company, and not what is actually important to the stakeholders. It has become quite a common practice for regulators and savvy investors to come to the conclusion that this is a red flag. The best practice is to have structured interviews or surveys with investors, customers, employees, suppliers and community representatives and to then map what they say in terms of what the business risks and opportunities are.

Assurance is one of the areas in which practice is developing rapidly and will be part of phase six. Many companies have released ESG data in the past without it being verified. Reporting is becoming a requirement in more jurisdictions and so is assurance. The difference between limited assurance (which offers a lower level of assurance and may require less level of testing) and reasonable assurance (which is equivalent in rigour to a financial audit) is a very important consideration when deciding the programme of an organisation’s reporting. Most companies start with limited assurance and progress to reasonable assurance as they continue to develop their data systems and internal controls. It is far more efficient to involve an external assurance provider early in the process (before the end of the reporting period) than at the end of the reporting period, when a lot of time is wasted re-stating data that is not of evidential quality.

What Is ESG Reporting: Conclusion

ESG reporting has firmly broken out of the silos and is now ingrained in corporate reporting. To those who are familiar with it, that transition presents real career opportunities: There is a huge need for individuals with the knowledge and skills needed to meld financial stringency and sustainability expertise, and the demand exists in every sector, role, and location.

If you are on a learning curve in this field, here are three practical steps that will speed up your learning curve. First, take time to get an understanding of the key frameworks on a conceptual level rather than trying to learn the technicalities of any one of the standards. If you have an understanding of how GRI, TCFD, ISSB, and CSRD fit into each other and what they are aiming for, you will have a mental map of their details that can be absorbed much more easily. It’s easy to see that, while there is a lot of logic left to be uncovered, the common elements in the ESG reporting framework across the various standards are quite similar; namely that materiality, data integrity and the documentation of methodology are all expected in the reporting. Secondly, learn practical data skills. The challenge of ESG reporting is not just a communications one, but a data management one. There are not nearly as many people around who can design the data collection process, identify and correct data quality issues, and create a simple tracking tool as there are people who can write sustainability narrative. Thirdly, seek a chance to collaborate or shadow with an ESG reporting consultant undertaking a genuine reporting exercise. The disparity between theory and practice in this area is significant, and nothing will help bridge it like exposure to the decisions, compromises and stakeholders of a real reporting process.

ESG reporting for companies is not a destination, but a journey that will build the skills needed to determine how companies will be assessed, financed and regulated for many years to come. The experts investing in that knowledge today will be better equipped to help in the decisions that will matter most.