ESG Compliance in Education Sector: Overcoming Reporting Barriers in Schools and Universities

Introduction to Professional ESG Education Reporting Course

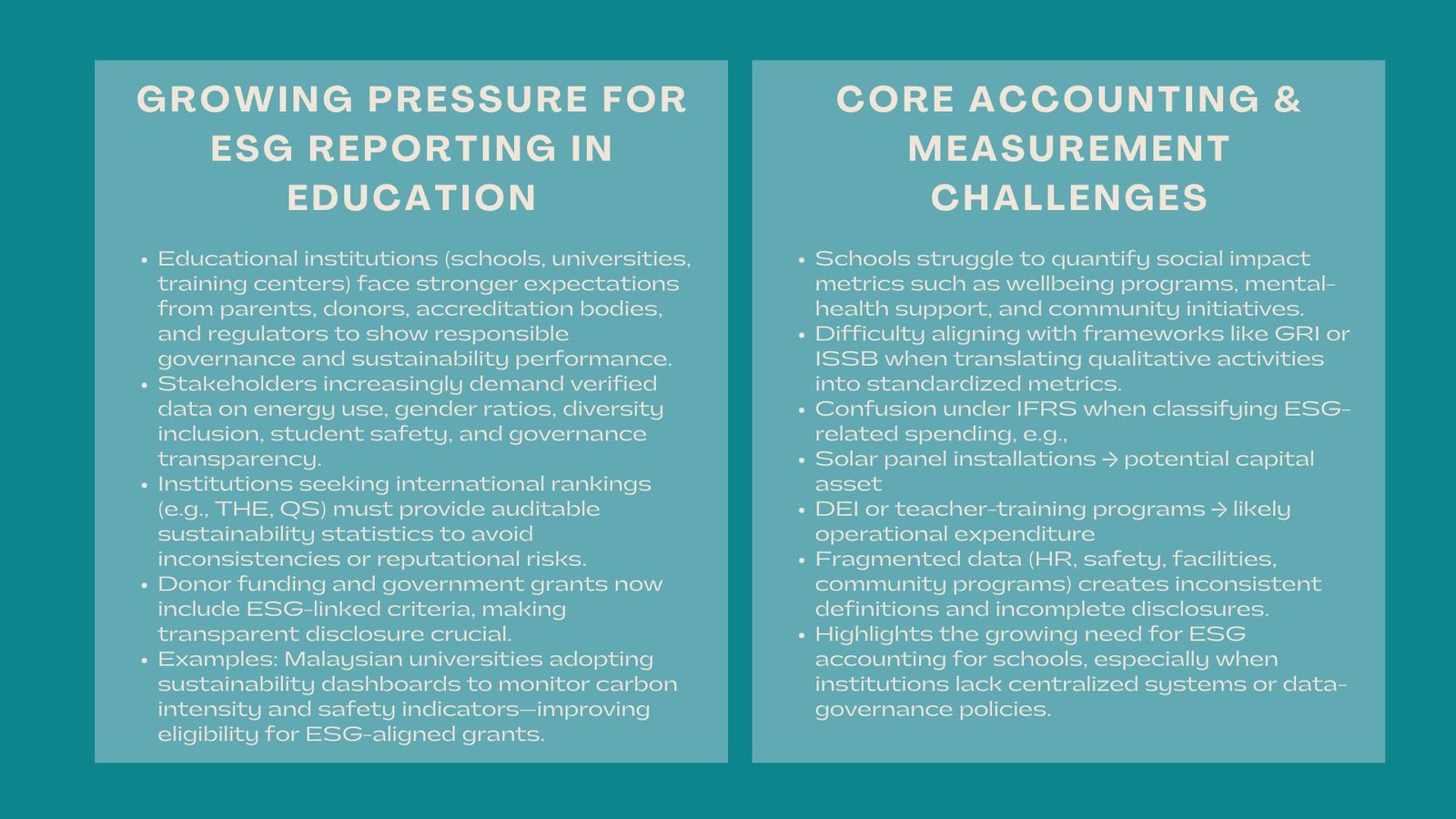

There is an increasing pressure on educational institutions, schools, universities, and training institutes, and vocational centers to express themselves responsible in terms of governance, environmental care, and social responsibility. Although most sectors have already incorporated the ESG embedded in the strategic decision-making process, education sector is still in its early stages of formalisation. This paper will look at one of the areas; the practical accounting and reporting challenges that schools go through when adopting ESG frameworks and how the schools can develop credible, audit-ready systems that would support the current transparency expectations.

1. The Increasing Demand to organize ESG Reporting in Education.

1.1 Increasing Stakeholder Expectations.

Parents, donors, accreditation organizations and regulatory authorities of the state are increasingly requiring transparency on the manner in which institutions handle the environmental impact, student welfare, community contributions, and financial management. This has tightened the Education ESG reporting requirements particularly to those institutions that want to acquire international accreditation or competitiveness funding.

As an illustration, when universities seek global ranking positions like THE or QS, they have to provide verified statistics on sustainability, e.g. energy consumption, gender balance rates, or diversity. Without a systematic reporting mechanism, the institutions also face the risk of inconsistent reporting or reputational disparity between those that are better armed with the mechanism.

1.2 Funding and Reputation Implication.

ESG-aligned reporting is usually demanded by international donors and government grants. Schools that are transparent in their governance and also have sustainability promises in their governance are more likely to gain trust and continuity in their donor relationships. On the other hand, irregular reporting may result in the generation of delayed funding or unsuccessful accreditation periods.

An example of this is the introduction of sustainability dashboards in multiple universities in Malaysia to track metrics of carbon intensity and safety of their students to receive future ESG-linked grants.

2. The Accounting Problems in the Educational ESG Reporting.

2.1 Problems with Measuring Social Impact.

The pillar of S is especially tricky on the part of schools since social outcomes, wellbeing of the students, engagement with the community, diversity inclusion, cannot be measured. The institutions need to balance between qualitative programs and quantitative reports.

One of the common issues is to record safeguarding policies or mental-health support programs in quantifiable terms, which may adhere to international standards, including GRI or ISSB.

2.2 Under IFRS Recognizing Costs ESG-Related.

Schools may also not be able to categorize the sustainability expenditures as stipulated by the IFRS, particularly on whether it should be considered as an operation or investment.

Examples include:

- Equipping with solar panels (potential capitalized asset with long-term returns).

- Conduction of teacher development programs, programs on DEI (operational expenditure).

These classification decisions have a direct effect on financial statements and valuation of long term assets.

2.3 Fragmented Data Sources

The student safety logs, energy data of facilities, HR diversity measurement, and community-engagement programs are usually in different departments and therefore difficult to consolidate.

Lack of central data governance leads to the possibility of duplication, difference in definition or missing disclosures.

The long-tail keyword ESG accounting for schools fits into this context, emphasizing how institutions often lack standardized methodologies for aggregating and verifying ESG-related financial and operational data.

3. Environmental Reporting Challenges in the Education Sector

3.1 Carbon Footprint Measurement

Schools and universities have facilities of large size such as classrooms, laboratories, cafeteria, transportation fleet among other facilities thus environmental reporting is imperative yet complex.

Common barriers include:

- Absence of automated metering systems.

- Problems with keep apart tenant vs. school utility use.

- Poor waste and recycling reporting.

Indicatively, one of the universities in Singapore conducted a pilot project on a building-level energy monitoring system to minimize variability, leading to improved reporting of Scope 1 and Scope 2 emissions.

3.2 The accounting of Green Infrastructure Investments

The institutions that invest in renewable energy equipment, green buildings, and water-saving systems need to find out whether they are depreciated assets, grants or financial instruments linked to sustainability.

Improper segmentation may lead to audit problems or nonconformity to sustainable financing standards.

4. Compliance and Governance Lapses.

4.1 Inequalities in Governance Structure.

Most institutions do not have ESG committees or a set of responsibilities. This results in a disjointed decision making and poor monitoring of risks, which are associated with sustainability like:

- Weaknesses in terms of data privacy.

- Student safety incidents

- Ethical procurement risks

Schools with decentralized governance face the most difficulty meeting Education ESG reporting requirements, especially when no department is responsible for validating ESG disclosures.

4.2 Ethical and Responsible Procurement

The institutions usually purchase food, uniforms, IT systems and structures. Unless the schools screen the vendors, they will end up contributing to the cause of bad laborers or environmental pollutants.

The adoption of the procurement scoring systems and Vendor risk mapping are becoming widespread in sophisticated markets like Australia and the UK.

5. Barriers to Social Metrics and Reporting.

5.1 Tracking Student Safety and Wellbeing.

The social impact of the education sector is spearheaded by wellbeing programs, anti-bullying policies, and services to boost mental-health. Nonetheless, there is always an issue with reporting them because of:

- Classification of sensitive data.

- Definition difference (e.g. what constitutes a safety incident)

- Inadequate digital reporting equipment.

A Malaysian group of private schools adopted an integrated safeguarding application to harmonize reporting to enable more precise ESG disclosures.

5.2 Diversity, Inclusion and Workforce Reporting.

Organizations are to report diversity ratios, pay equity, and non-discriminatory hiring. However, the past HR systems may not permit retrieval of clean and comparable data.

The current HRIS systems feature sustainability tagging, which assists schools to produce ESG workforce reports.

6. Creating a Sustainable ESR Reporting Framework in Education.

6.1 Installing the Internal Controls and Data Centralization Systems.

Individual schools need to bring on board cohesive reporting systems that bring together financial, environmental, and social information. The indicators that can be tracked on a real-time basis, including energy usage, student safety records, and workforce indicators, could be monitored with the help of a centralized data governance structure.

6.2 Fitting into Global Standards.

Structured templates such as Frameworks such as the Global Reporting Initiative, ISSB Standards and regional ESG taxonomies can be implemented by schools. Organizations that have cross-border programs are the ones that gain the most in the standardized environment which lessens disparities in reporting.

6.3 Upskilling Administrative and Accounting Personnel.

ESG accounting demands proficient skills not only technical accounting skills but also knowledge in the field of sustainability frameworks. In order to enhance the level of compliance, some universities have begun dispatching ESG-oriented training on the IFRS of finance teams.

Conclusion: Making Education Future-Ready in terms of ESG.

Due to the increase in transparency expectations, ESG reporting is no longer something that educational institutions may consider optional. Accurate systems that are in compliance with the standards can assist schools to attract funding, enhance their governance, as well as develop confidence with their parents, regulatory bodies, and accreditation organizations. The trends in the future lean to the creation of digital ESG dashboards, multifunctional accounting platforms, and obligatory reporting requirements even in private and non-profit institutions.

The competitiveness, credibility, and role played by the education sector towards the wider society will be based on its competence to embrace acceptable ESG accounting practices