ESG Reporting Trends in Manufacturing

Introduction to Improving ESG Reporting in Manufacturing

The manufacturing business is at the threshold of change. Having previously focused on the productivity and cost-effectiveness, the current manufacturers are now under the great pressure to act sustainably, openly and in a responsible way. The transformation of environmental, social and governance (ESG) performance measurement and reporting is occurring as a result of global supply chains, investor demands, and regulatory requirements.

ESG reporting is not just a symbolic act or a marketing program anymore, it is an important measure of corporate health. To manufacturers, ESG disclosures can affect all aspects of financing opportunities and investor trust, operational efficiency and brand resilience. This paper will center on the current trends in the emergence of ESG reporting that is reshaping the manufacturing industry and how firms are streamlining their operations towards the principles of sustainability, enhancing their valuation and satisfying the global need of accountability.

1. The Emergence of ESG Reporting in the Manufacturing Industry.

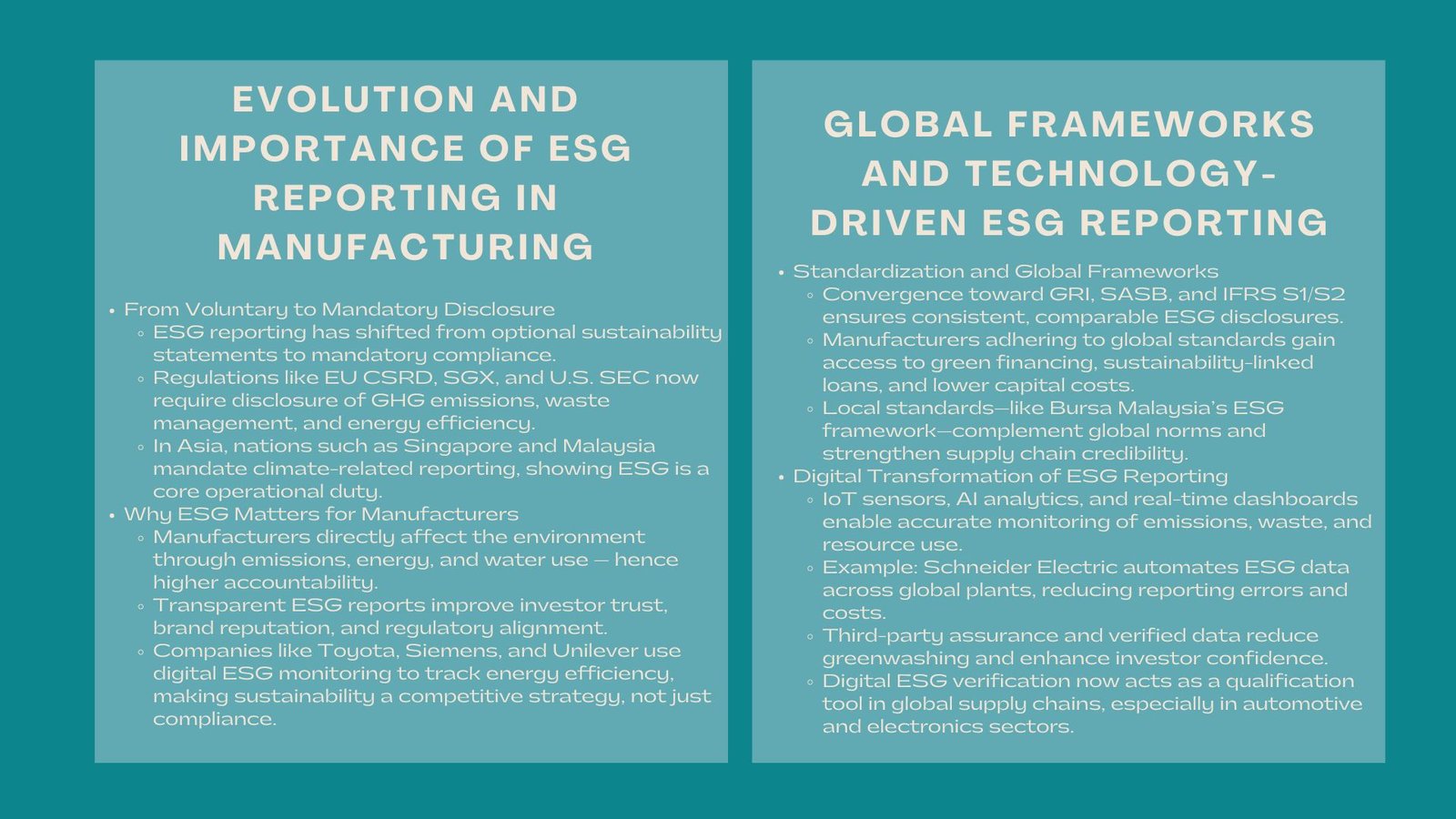

1.1 Voluntary Disclosure to Regulatory Obligation 1.2.

In the last ten years, producers have no longer been engaged in voluntary disclosures of sustainability but now mandatory reporting on ESG. New and stricter ESG disclosure regulations are being enforced by regulatory authorities, including the European Union (in the form of the Corporate Sustainability Reporting Directive), Singapore Exchange (SGX), and the U.S. Securities and Exchange Commission. This evolution has made Manufacturing ESG compliance standards a central consideration for global and regional firms.

A scheme to compel manufacturing companies to report on environmental performance indicators such as greenhouse gas (GHG) emissions, waste management, and resource efficiency in their annual reports is being adopted in Asia by such countries as Singapore and Malaysia. This is an indication of a definite change: sustainability is no longer a fringe benefit, but rather a working requirement.

1.2 Why ESG is More Important to Manufacturers.

The influence of manufacturers on the environmental resources is direct and measurable, energy consumption, water consumption, and emissions are all objective aspects. This is known by the investors and regulators; this is why they require more transparency in this sector. ESG reporting enable manufacturers to indicate proactive environmental management, social responsibility and governance ethics which all influence long term competitive advantage.

As an example, such corporations as Toyota, Siemens, and Unilever have focused sustainability in their manufactures and apply digital monitoring instruments to monitor the emissions and energy efficiency. Their reporting on ESG is not a mere report compliance but also a key strategy of reinforcing their international brand reputation and relationship with investors.

2. The changing Frameworks and Standards.

2.1 The Global Reporting Shift

ESG reporting is a fast-evolving world that is headed to harmonization. The Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), as well as the IFRS Sustainability Disclosure Standards (IFRS S1 and S2) are currently being used to help manufacturers standardize their ESG-related indicators. These reporting systems offer similar and trustworthy information to investors, regulators, and customers.

Companies that conform to these universal standards can enjoy the benefit of availability of sustainable financing and global trade opportunities. An effectively prepared report on ESG can open green bonds, seek sustainability-based loans, and even lower capitals by gaining investor confidence.

2.2 Standards regionally and implementation locally.

International systems form a framework, however, domestic manufacturers have to comply with local regulations. In Singapore, the priorities of ESG reporting among manufacturers are climatic resilience and disclosure of emissions. The Bursa Malaysia Sustainability Reporting Framework in Malaysia urges firms to release their social and governance measures.

Adherence to these local standards does not only provide regulatory conformity, but it also enhances competitiveness in any supply chain because buyers of goods all over the world are now more willing to deal with suppliers who are certified to comply with the ESG standards.

3. ESG Reporting which is technology-driven.

3.1 The Role of Digitalization

The digital transformation is reworking the ways manufacturers handle ESG data. Contemporary production plants now incorporate sensors, IoT, and AI-powered analytics to be able to track real-time emission, waste, and energy usage. These data feeds directly into ESG reporting dashboards, which make it accurate and timely.

To illustrate, the Schneider Electric has invented an automated system of collecting ESG data that pulls together hundreds of metrics of sustainability across its production locations across the world. This digital integration does not only ease the compliance but also decreases the cost of reporting, and human error.

3.3 Data Safety and Protection.

As questions on ESG claims are increasing, companies are being eager to purchase third-party certification to certify their reports. Credibility and minimization of greenwashing claims are guaranteed by independent audits and verified metrics. Shareholders are increasingly asking that sustainability information be treated similarly to financial information, as verifiable information, and this trend is changing the culture of corporate reporting.

Supply chain relationship is also enhanced by third-party assurance. An authenticated ESG report might be utilized as a qualification instrument of partnering with mega purchasers, particularly in sectors such as automobiles, electronic, and consumer goods.

4. Connection between ESG Reporting and Financial Valuation.

4.1 ESG as a Corporate Value Generator.

Among the most interesting developments in the contemporary manufacturing sector, one can distinguish the direct correlation between ESG reporting and corporate valuation. Investors have changed the way companies are valued by analyzing financial performance in terms of sustainability aspects which now influences mergers, acquisitions and equity markets.

Companies that have been observed to make sustainable strides are likely to be valued highly, experience reduced borrowing rates, and improved credit ratings. An example is that companies that report their robust performance on emissions mitigation or integration of renewable energy is now being increasingly rewarded by investors who want to have low-risk and future-focused portfolios

This growing emphasis underscores the importance of ESG valuation for manufacturers—a process that translates sustainability achievements into measurable financial value. It enables companies to measure the value of ESG activities in terms of profitability, brand reputation and risk management.

4.2 ESG Opportunity and risks of valuation.

The non-disclosure of ESG metrics may prove to be costly. Manufacturers with no open reporting have a cost of financing, diminished interest by investors and a risk of being more regulated. Conversely, the ones that have the lead in ESG reporting would be in a position to attract green investors and long-term institutional funds.

As an illustration, the focus of the major investment funds like BlackRock and Temasek Holdings is to focus on companies that have detailed ESG disclosures. Their investment criteria would tend to measure the thoroughness of ESG reporting and plausibility of sustainability objectives.

5. ESG Reporting Trends in the Future of Manufacturing.

5.1 The scope 3-Emissions and Supply chain Accountability deals with emissions and CVS related to the supply chain.

In coming 10 years ESG reporting in manufacturing will have the Scope 3 emissions which are the indirect emissions, those that occur along the supply chain. Such a change will necessitate increased cooperation between manufacturers, suppliers, and logistics partners to achieve end-to-end transparency.

Manufacturers will be required to monitor carbon emission in their activities, as well as the activities of the upstream and downstream companies that lead to their environmental presence. The extended range will complicate and increase the effectiveness of ESG data collection in the presentation of holistic sustainability performance.

5.2 Integration of ESG into Enterprise Strategy

ESG will cease to remain a standalone reporting activity-it will be a part and parcel of business strategy. The sustainability goals are already being connected with product innovation, cost reduction, and market differentiation by manufactures. ESG performance measures are becoming more related to executive compensation, corporate governance indicators and long-term planning.

The integration will assist manufacturers to move away the reactive compliance to proactive sustainability leadership and will make them one of the first in the global switch to responsible industry.

Conclusion

With the emergence of ESG reporting as a core of the manufacturing industry, competition, and interactions with the stakeholders, the sustainability maturity of the sector will define its long-term sustainability. To have authentic, data-informed ESG reporting that addresses both international and domestic regulations has become a competitive benefit.

Companies that share this change – acting in accordance with the Manufacturing ESG compliance criteria; incorporating ESG manufacturer valuation in their financial decision-making – will be the first to set the stage of the next stage of the evolution of industry. ESG is not now a mere reporting tool, but it is the building block to the future in which profitability and responsibility are joined at the hip.