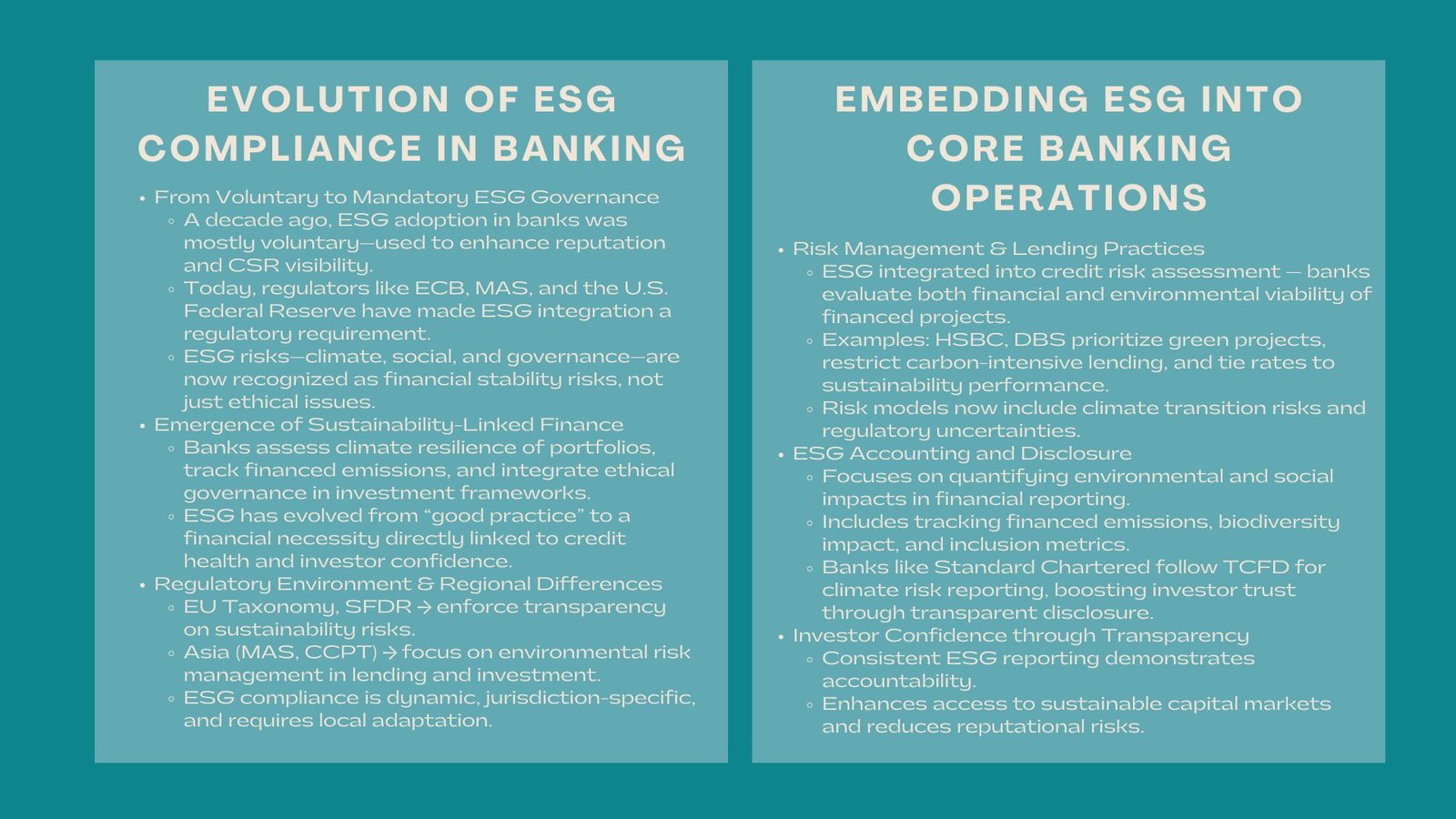

ESG Compliance in the Banking Sector

Introduction to ESG Compliance Trends in Banking

Over the past few years, the principles of Environmental, Social and Governance (ESG) have ceased to be a voluntary ethical guideline, but a compulsory compliance policy of all international financial systems. To banks, this is not merely a reputation issue, but an issue of regulatory survival, investor trust and permanence. Banks are under increasing pressure on the part of regulators, stakeholders and investors demanding that they transparently incorporate ESG into credit policies, lending practices, and governance practices. With the world economy turning towards sustainable finance, the capability of the banking industry to adhere to the ESG sets will dictate the competitiveness of the financial industry, capital accessibility, and credibility. This paper discusses the most vital aspects of ESG compliance in banks, the current changes in regulations, and their strategic consequences to financial institutions across the globe.