MAS Guidelines on Environmental Risk Management for Financial Institutions

Introduction to MAS Environmental Risk Management Guidelines

The Monetary Authority of Singapore (MAS) has made a bold stride in the quest by Singapore to be a global leader in sustainable finance through formulating detailed expectations regarding the manner in which financial institutions ought to treat environmental risks. These rules are a significant step in the development of the financial ecosystem in Singapore – instead of short-term profitability, the emphasis on sustainability over the long term.

Environmental risk is no longer a peripheral issue in the case of banks, insurers and asset managers. It is one of the crucial factors of credit quality, returns on investment, and resilience in operations. The MAS Guidelines on Environmental Risk Management is a pillar in trying to make sure the financial sector incorporates sustainability in its decision-making procedure- ensuring financial soundness and environmental wholesomeness.

Learning about MAS Environmental Risk Management Framework.

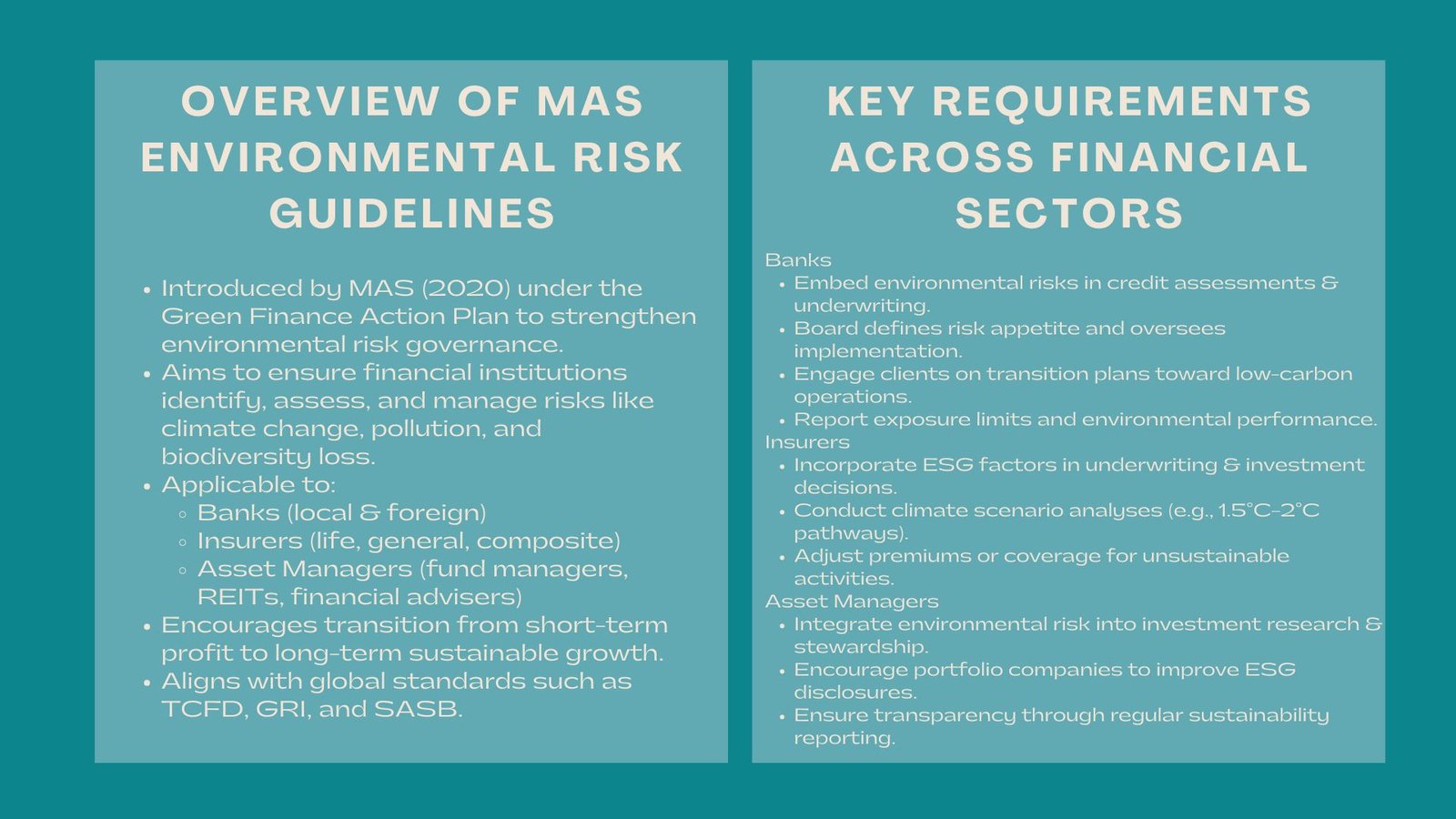

In 2020, the MAS environmental risk management guidelines were established to manage the environmental risks of banks and financial institutions in Singapore as part of the Green Finance Action Plan of the country. These principles are to ensure that the financial institutions identify, assess and limit the environmental risk like the climate change, depletion of biodiversity and pollution.

The MAS claims that the most likely adverse impact on the financial situation of the institution caused by the environment is the environmental risk. These risks can be physical e.g. floods or wildfires, transition e.g. a shift in regulations or a shift of consumer preference to greener products.

The adoption and implementation of environmental risk management in financial systems with the assistance of MAS will create a strong and progressive financial industry that will be able to sustain low-carbon transition in Singapore.

MAS Guidelines Objectives.

The major aim of these guidelines is to persuade the financial institutions to consider the environmental risk as part of their governance, strategy and risk management procedures. This will ensure that sustainability is not taken as a PR campaign, but as a business risk.

Particularly, the guidelines are expected to:

- Enhance the resilience of financial institutions to the environmental shocks.

- Optimize the financial sector in Singapore according to the international standards of sustainable finance.

- Enhance the investment in economic activities that are environmental friendly.

- Ensuring that there is transparency and accountability in environmental risk disclosures.

Scope of Application

The rules are applicable to three principle types of regulated financial institutions:

- Banks – foreign bank branches, local full banks.

- Insurers – these include life, general and composite insurers.

- Asset Managers – licensed fund management companies, REIT managers and financial advisers.

All the institutions are supposed to shape their environmental risk management practices to the nature, scale and complexity of its operations.

Key Requirements for Banks

In this respect, banks are also very vulnerable to environmental risks because investments through lending portfolios are usually very important in financing economic activities. Banks under the MAS guidelines have to incorporate the environmental consideration in the credit risk assessment and underwriting processes.

Governance and Oversight

Board of directors role: The boards of directors should set the environmental risk appetite on top-down, by defining the environmental risk appetite of the bank and by controlling the implementation of policies. The top management should make sure that the personnel are properly trained and the internal procedures are in accordance with MAS expectations.

Risk Identification and Evaluation.

Banks should determine the most vulnerable clients and employment sectors to the environmental risks e.g. energy, agriculture or manufacturing. The risks are supposed to be included in the credit approvals and monitoring.

Due Diligence and Engagement.

Banks are also advised to consult their clients regarding their environmental practices before granting them more financing. This also involves the consideration of the credibility of transition plans by the borrowers towards the low-carbon operations.

Portfolio Management and Reporting.

Banks are advised to track the environmental risk profile of their loan books, establish exposure limits where the need be, and report on how they have managed them in their sustainability reports.

Important Prerequisites of Insurers.

The insurers are vulnerable to environmental risks both in their portfolios and underwriting. The MAS guidelines also demand that they should take into account the environmental risks in a three-dimensional format, underwriting, investments, and operations.

Underwriting Policies

Environmental factors should be considered by the insurers when pricing the policies or covering especially in high impact areas such as energy and transportation. To illustrate, the insurers can change premiums or provide no coverage to the unsustainable activities.

Investment Strategies

To protect the value of the portfolios, the insurers should incorporate environmental risks in their investment choices. It can be screening investment on climate risks or reducing investments in green assets.

Scenario Analysis

MAS is urging insurers to undertake climate scenario analysis to remind them how their portfolios would react to a range of climate scenarios, including a 2degC or 1.5degC scenario

Key Requirements for Asset Managers

Asset managers play a pivotal role in channeling capital toward sustainable investments. Under the MAS environmental risk management guidelines for banks and financial institutions in Singapore, asset managers must embed environmental risk considerations across their entire investment lifecycle.

Investment Research and Due Diligence.

Fundamental analysis should include evaluation of environmental risks. Managers need to consider the impact of environmental practices of companies in long-term value creation and exposure to risk.

Stewardship and Engagement

Asset managers are motivated to discuss with portfolio companies the performance of ESG and promote improved disclosure and governance. Active stewardship is considered an effective tool to trigger positive change.

Disclosure and Transparency.

Managers have to report on the way they deal with the environmental risks in their portfolios and this will provide investors with insight on how they approach sustainability.

Good Governance and Accountability.

Governance is one of the fundamental elements of the expectations of MAS. The top management and the board of directors should be the ultimate owners of the environmental risk management.

- Board should establish explicit sustainability goals, risk tolerance and accountability measures.

- The senior management has the mandate of operationalizing policies and making them part of the day to day business operations.

- The effectiveness of environment risk management frameworks should be periodically checked by internal audit functions.

This is because during a strong governance, there is no third party who ignores environmental risks but makes sure that these risks are systematically factored in when making business decisions.

Expectations of Disclosure and Reporting.

The transparency is a vital element of the MAS guidelines. The financial institutions are required to provide meaningful information on the way they deal with environmental risks. This includes:

- Risk governance frameworks and policies.

- Environmental risk assessment techniques.

- Sustainability performance related metrics and targets

- Inclusiveness of the ESG factor in lending, investment and underwriting.

MAS encourages alignment with international disclosure standards, such as the Task Force on Climate-related Financial Disclosures (TCFD), to ensure comparability and consistency.

Sustainable Finance and Compliance

The sustainable finance and environmental risk compliance under MAS regulations in Singapore has broader implications beyond risk management—it positions Singapore as a leader in green and transition finance.

Financial institutions can also align capital and investments with the carbon neutrality, renewable energy, and climate resilience by incorporating the principals of ESG in their credit and investment decisions.

Such a strategy not only increases compliance but also opens the doors in green bonds, sustainable infrastructure and climate-resilient investments.

MAS has encouraged such efforts by means of initiatives like:

- Green and Sustainability-Linked Loan Grant Scheme (GSLS).

- Singapore Green Finance Centre Partnership in sustainable finance education and research.

- The Singapore-Asia Taxonomy of sustainable economic activities.

The combination of these efforts strengthens the Singapore vision of the green finance hub at the regional level.

Implementation problems

Although the framework offers a good direction, there are a number of challenges associated with its implementation in institutions:

- Data gaps: Data on the environment is not always reliable, particularly in the case of a private company.

- Scenario uncertainty: It is not yet well understood how to predict the long-term effects of the climate.

- Lack of talent: The need to find professionals who are knowledgeable about ESG and sustainable finance is increasing.

To address these challenges, financial institutions are investing in the ESG analytics tool, capacity building and cross sector collaboration.

Conclusion

The MAS Environmental Risk Management Guidelines of Financial Institutions bring a significant change in the financial environment of Singapore. With the inclusion of environmental considerations in the governance, credit and investment practices, MAS achieves the result of making sustainability a core element of risk management and strategic planning.

With the world moving to the low-carbon future, the strategy of Singapore, which rests on clarity of its regulations and proactive oversight, positions Singapore as an example of how profit and purpose can be harmonized in financial systems.

By doing so, financial institutions which are prompt and implement strong environmental risk frameworks will not only remain in line but will also be the pioneers of sustainable finance in the region of Asia and other parts of the world.