Sustainability Reporting of Companies: Principles, Processes, and Regulatory Requirements Explained

Introduction to Apply Sustainability Reporting Compliance Principles

In recent years, sustainability has moved from a peripheral corporate concern to a central pillar of business strategy, governance, and risk management. Investors, regulators, customers, and employees increasingly expect organizations to demonstrate accountability not only for financial performance but also for environmental, social, and governance impacts. This shift has made sustainability reporting of companies a critical mechanism through which organizations communicate their long-term value creation and resilience.

This article provides a comprehensive and practical explanation of sustainability reporting what is it, focusing on how companies design, implement, and comply with structured reporting frameworks. It examines the sustainability reporting principles and process, explores evolving sustainability reporting requirements, and illustrates how companies across industries integrate sustainability disclosures into corporate decision-making. The discussion is intended for business leaders, finance professionals, compliance officers, and sustainability practitioners seeking a clear and authoritative understanding of this increasingly mandatory corporate practice.

1. Sustainability Reporting: Concept and Strategic Importance

1.1 Sustainability Reporting: What Is It in a Corporate Context

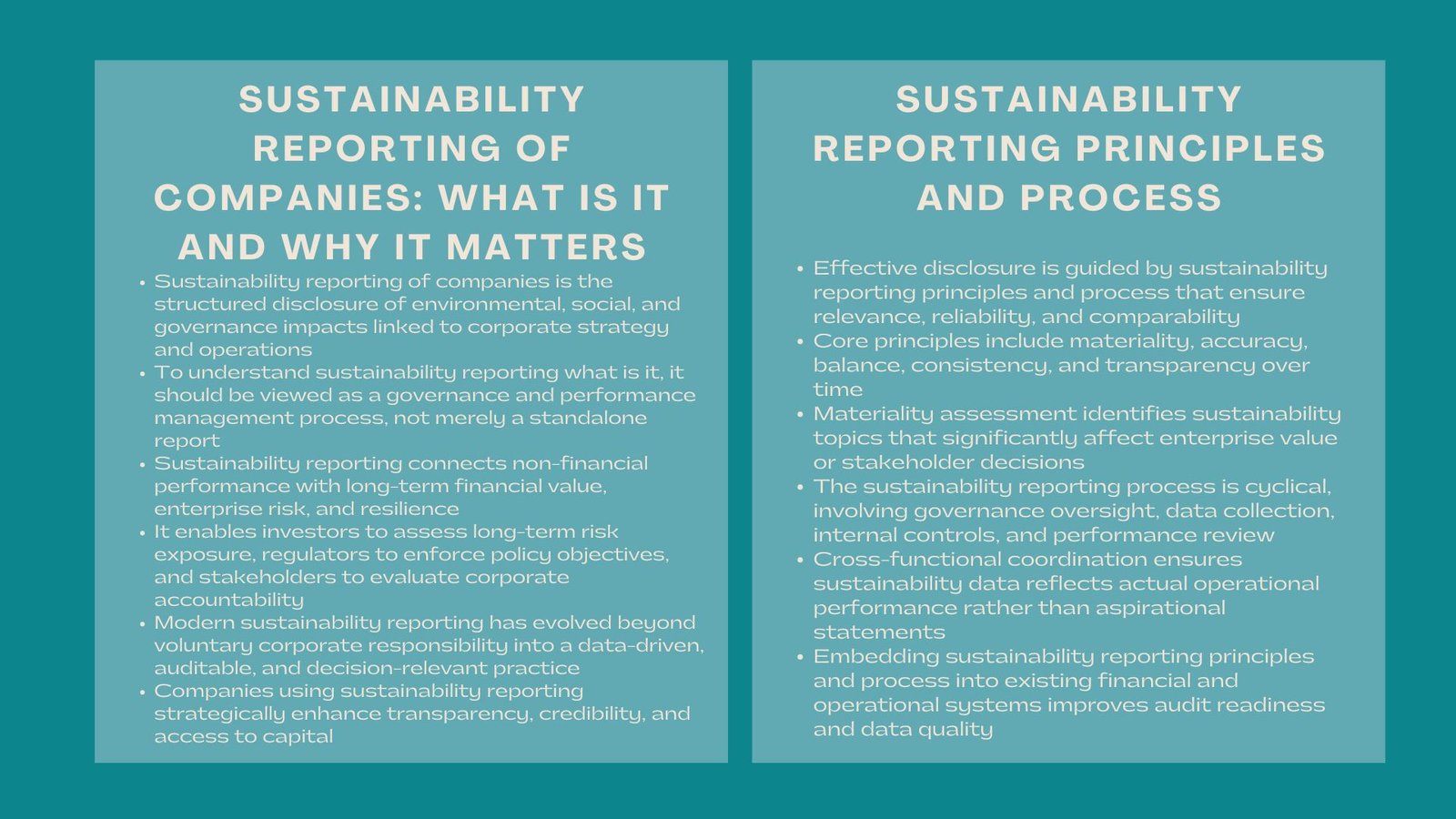

In order to comprehend sustainability reporting what is it, a person has to go beyond the publication of a separate report. Sustainability reporting is the organized reporting of how an organization determines, controls and quantifies its environmental, social and governance effects concerning its strategy and operations. It links the non-financial performance and long-term financial outcomes and risk management.

To contemporary organizations, the idea of sustainability reporting of companies has ceased being restricted to the story of corporate social responsibility. Rather, it is now a process that is data-driven, governance-led to promote transparency, comparability and accountability. Companies are currently relying on sustainability reporting to show how they are handling climate risk, labor practices, supply chain integrity, data protection, and ethical practices in a quantifiable and audit-able way.

1.2 Why Sustainability Reporting Matters to Stakeholders

Sustainability reporting is significant as a strategic tool of decision making by the stakeholders. Sustainability disclosures are becoming more important to investors as a measure of long-term risk exposure and capital allocation choice. The regulators rely on the sustainability data to implement policy goals involving climate change, social protection, and corporate accountability. Sustainability transparency, in turn, is considered by customers and employees as a sign of corporate values and credibility.

This directly affects reputation, access to capital and competitiveness as a result of sustainability reporting of companies. Companies that consider sustainability reporting as a strategic business practice instead of a compliance chore are in a better position to streamline their long-term development in line with the expectation of the stakeholders.

2. Sustainability Reporting Principles and Process

2.1 Core Sustainability Reporting Principles

Effective disclosure has its basis on the sustainability reporting principles and process embraced by an organization. These principles lead to the way of identifying, measuring, and presenting information to make sure that sustainability reports are decision-related and plausible. Basic principles are generally materiality, accuracy, balance, consistency and comparability across time.

Of specific interest is materiality. Business organizations are required to determine topics on sustainability that may significantly affect the stakeholder choices or enterprise value. This, in practice would involve structured tests including the internal management, external stakeholders and risk analysis. Introducing the concept of materiality into the sustainability reporting principles and process, companies do not have to resort to generic reporting instead of addressing the issues that are of interest to their business model.

2.2 The Sustainability Reporting Process in Practice

Sustainability reporting principles and process does not just stop at writing a report. They encompass a cyclic process of governance control, data gathering, internal controls and performance check. The major organizations are incorporating sustainability reporting in the current financial and operational systems and therefore data flows are trustworthy and auditable.

As an example, an industrial organization can create cross-functional teams to monitor emissions, workplace safety rates, and compliance information of suppliers. Shareholders scrutinize these inputs by means of internal governance committees and then make a formal disclosure. This is a systematic procedure that makes sustainability reporting of firms capture real performance of operations as opposed to the idealistic statements.

3. Sustainability Reporting Requirements and Regulatory Landscape

3.1 Evolution of Sustainability Reporting Requirements

The sustainability reporting requirement has grown tremendously, in the last 10 years, due to the world wide climate promises, shareholder activism, and regulatory changes. What was formerly to a large extent voluntary has become obligatory in most jurisdictions. Regulators have now mandated companies to report sustainability risks and financial effects of climate changes and governance practices in a standardized format.

Sustainability reporting has brought about a greater role of the finance and compliance functions in sustainability reporting due to the increasing complexity of its requirements. Organizations have to ascertain coordination of disclosure of sustainability and financial reporting, especially in the cases when climate risks and social factors can influence the value of assets, provisions, and future cash flows.

3.2 Mandatory Versus Voluntary Sustainability Disclosures

Although certain sustainability disclosures are voluntary, a number of sustainability reporting regulations have come to force in the listed companies, large privately owned organizations and regulated industries. Such requirements frequently stipulate reporting requirements, assurance expectations and accountability at the board of directors.

Practically, those companies that actively implement effective sustainability reporting frameworks are in a better position to face the changes in regulations. Early adoption minimizes the chances of non-compliance and facilitates the implementation of reporting requirements as they increase. This preventative strategy enhances the general credibility of sustainability reporting of the companies with the eyes of the regulators and investors.

4. Governance and Internal Accountability in Sustainability Reporting

4.1 Board and Management Responsibilities

The sustainability reporting of the firms requires effective governance structures. The boards are taking more responsibility to monitor sustainability strategy, risk management and reporting integrity. This control is to make sure that the disclosure of sustainability is in line with corporate objectives and risk appetite.

Senior management is vital in the implementation of the sustainability reporting principles and process in the units of business. By putting in place accountability on the ownership of data and performance objectives, organizations instill in their day-to-day decision-making a sense of sustainability as opposed to it being an independent reporting practice.

4.2 Integration with Enterprise Risk Management

Enterprise risk management is closely associated with sustainability reporting. All these risks, climate risks, human capital challenges and regulatory compliance risks, can have financial implications. Through incorporating sustainability concerns in the risk structures, companies can make sure that reports on sustainability reporting basis are based on sound analysis.

This helps in the strength of sustainability reporting what is it as a prospective management tool and not a backward story.

5. Industry Applications and Real-World Examples

5.1 Sustainability Reporting Across Sectors

The level of sustainability reporting of companies diffuses according to the industry. The disclosures in energy and utilities are sometimes focused on the emissions, transition strategies, and capital investments in renewable technologies. In financial services, the focus of sustainability reporting is on responsible lending, governance and exposure to the climate-related financial risks.

Compared to manufacturing and consumer goods companies, they can focus on the supply chain transparency, labor practices, and product lifecycle impacts. Although there are such differences, the fundamental principles and process of sustainability reporting are the same in all sectors.

5.2 Value Creation Through Sustainability Reporting

Practical experience demonstrates that those companies that strategically use sustainability reporting tend to gain tangible benefits. Increased transparency will increase investor confidence whereas structured data on sustainability will justify operational efficiencies and cost savings. In the long run, good disclosures on sustainability lead to better access to capital and reduced risk premiums.

These results indicate that adherence to the requirements of sustainability reporting can be associated with the creation of value in the event that sustainability is part of corporate strategy.

6. Data Quality, Assurance, and Technology

6.1 Ensuring Data Reliability in Sustainability Reporting

With the increased regulation of sustainability disclosures, the quality of data has become an important issue. The companies should make sure that sustainability metrics are valid, consistent and should be backed by internal controls. This need supports the essence of institutionalizing the principles and the process of sustainability reporting in the governance systems.

The credibility of sustainability reports is becoming more and more attached to the assurance provided outside of the company. Independent verification gives the stakeholders a feeling that the disclosures are credible and do not reflect material misstatements.

6.2 Role of Technology in Sustainability Reporting

Digital platforms and analytics now assume a huge role in the sustainability data management. These tools allow companies to gather, calculate, and report sustainability indicators in an effective way in the global operations. Scenario analysis and disclosures ahead are also aided by technology, as necessitated by the emerging sustainability reporting requirements.

Technology also reinforces the role of sustainability reporting of companies as a strategic management activity as opposed to a compliance activity that is manual.

7. Challenges and Future Direction of Sustainability Reporting

7.1 Common Challenges Faced by Companies

Sustainability reporting remains a problem to companies despite the improvement. These are the changing regulations, inconsistency of data availability, and the requirement to strike a balance between transparency and commercial sensitivity. To deal with these challenges, there is a need to continuously improve the sustainability reporting principles and process.

Companies that invest in governance, training and systems are in a better position to move through these complexities and continue to be compliant to the evolving requirements of sustainability reporting.

7.2 The Future of Sustainability Reporting

In the future, it could be predicted that sustainability reporting will be more fully integrated with financial reporting. The difference between financial and non-financial reporting is going to be mitigated as the stakeholders insist on greater connections between sustainability performance and financial results.

This development supports the topicality of the sustainability reporting what is it as an essential part of corporate responsibility and the long-run value generation.

Conclusion

The growing emphasis on sustainability has transformed corporate disclosure practices worldwide. Sustainability reporting of companies is no longer optional or symbolic; it is a structured, regulated, and strategic process that supports transparency, risk management, and stakeholder trust. By understanding sustainability reporting what is it, organizations can move beyond compliance and leverage sustainability reporting as a tool for strategic decision-making.

A robust approach grounded in clear sustainability reporting principles and process, aligned with evolving sustainability reporting requirements, enables companies to demonstrate resilience and long-term value creation. As regulatory expectations and stakeholder scrutiny continue to increase, organizations that embed sustainability reporting into governance and operations will be best positioned to succeed in an increasingly sustainability-driven business environment.